I have an announcement to share with you all today. I've decided to migrate my blog from blogspot to a new home on Substack (https://marketobserver.substack.com). This move will allow me to provide you with an enhanced reading experience and more engaging content.

Why the move? Substack offers a range of features that will help me deliver better content to you, including improved formatting, easier subscription management, and a more interactive community space. I believe this transition will benefit us all in the long run.

What does this mean for you?

New URL: Our new blog address is https://marketobserver.substack.com. If you are keen, please bookmark this new address!

All future articles will be published on Substack.

If you like my articles, please subscribe to our new Substack page so that you don't miss new ones.

Here is the first article that I have already published on Substack. It's titled "The Feedback Loop: George Soros' Reflexivity" and delves into an intriguing economic concept that deepened my understanding of Mr Market. You can read it here:

I hope you can find time to check it out. Let me know your thoughts!

While this will be my last post on this Blogspot platform, it's just the beginning of my journey on Substack.

See you there!

P.S. If you like my articles so far, please don't forget to subscribe to (https://marketobserver.substack.com) to stay updated with all my future posts!

This article tackles a topic that should be on everyone's mind: scams. Protecting ourselves and our loved ones is paramount, especially given the alarming rise of scams in recent years. This issue hits particularly close to home for me because I have elderly dependents who are prime targets for these heartless criminals. If they fall victim, their problem becomes my problem.

All of us will retire one day. For retirees with no active income, the consequences of being scammed are devastating. The loss of their hard-earned savings could mean sacrificing essential needs or even facing financial ruin.

What's even scarier? It's not only retirees who are vulnerable. ANYONE CAN BE SCAMMED. I've seen online forums like hardwarezone, where people deride scam victims as stupid and careless. "Basic smartphone safety practice also don't know. Already say many times don't anyhow click on suspicious links on Facebook advertisements liao. Stupid no cure."

Some people think they are too smart to fall prey to scams but this "it-won't-happen-to-me" attitude is dangerous.

While younger, tech-savvy individuals may not fall for phishing links, they can be scammed in countless other ways. Everyone has unique weaknesses and vulnerabilities. Once a scammer identifies and exploits them, anyone can fall prey. I constantly remind myself not to be overconfident. After all, there are countless examples of more brilliant, more successful people who have been scammed.

Take the case of Nina Wang. At the time of her death in 2007, she was the richest woman in Asia, having amassed a fortune through her business acumen and fierce determination. She built her empire, Chinachem Group, alongside her husband, Teddy Wang, before his kidnapping in 1990. She famously stared down the kidnappers, paying a $33 million ransom, but Teddy was tragically never seen again. She even fought a high-profile legal battle against her own father-in-law for control of the company, ultimately solidifying her position as a business titan. If anyone seemed impervious to manipulation, it was Nina Wang. Yet, even she fell prey to a shocking scam.

The details of the scam seemed absurd, considering her business acumen. The scammer, Tony Chan, exploited Nina Wang's deep love for her late husband, Teddy Wang, and her loneliness as a widow. Teddy had disappeared years earlier after being kidnapped, and despite evidence pointing to his death, Nina refused to believe the evidence and clung to the hope that he was still alive. Tony, a self-proclaimed feng shui master, exploited this vulnerability by claiming he could locate her husband through his Fengshui's rituals. His rituals involved erotic massage. One thing led to another (use your own imagination). The two became lovers later. When Nina passed away, the scammer forged a will and named himself the sole beneficiary of her massive fortune. Justice prevailed and he was sentenced to 12 years jail for the forgery.

Nina Wang's story is a powerful reminder that even the smartest, most successful individuals are vulnerable to manipulation. If it can happen to her, it can happen to anyone of us. We all have emotional needs, blind spots, and moments of weakness that a skilled manipulator can exploit. Therefore, we must remain vigilant. Cultivating self-awareness, questioning motives, and seeking independent verification, especially when it comes to matters of the heart and finances, are crucial defenses against deception.

At the risk of sounding repetitive, there are 2 points which I want the reader to take away from this article.

Anyone can be scammed. Don't let overconfidence make you a target.

Be acutely aware of our vulnerabilities so that we can sense manipulation as it happens

Psychological manipulation extends beyond scams.

Be aware of it in sales and marketing to avoid being manipulated into buying unnecessary things.

Be aware of it even in personal relationships where toxic people manipulate you into doing things you don't want for their selfish interest.

Acknowledging our vulnerabilities and staying vigilant against manipulation are vital aspects of protecting ourselves and our wealth.

Here are the results of financial markets that I tracked in 2023, using tools I developed for personal use. The links to the tools will be provided. I have uploaded them to Github Pages and they are available to the public free of charge, with no advertisements.

Stock indices performances are reported after adjusting in USD for fair comparison.

The top 20 stock indices were all positive, with Nasdaq100 at the top gaining 53.81%. A In 2022, Nasdaq100 was the 2nd worst stock index at -32.97%. It was a strong rebound for Nasdaq100 in 2023.

Japan Nikkei225 gained 28.24% in nominal terms in 2023 and would have been ranked 2nd best performer on this metric. However, after adjusting for USD, Nikkei225 gained "only" 19.24% and the ranking dropped to 15th.

Japanese Yen depreciated against USD by 7.02%. When investing in Japanese stocks, the depreciating effects of the Yen cannot be ignored.

Bottom ranking of stock indices in 2023 (USD-adjusted)

The past 2 years(2023, 2022) have been terrible years for China/HK's stock markets.

China's ChiNext index is China's version of the U.S's Nasdaq index. The purpose of ChiNext index is to track high-growth, innovative stocks on the Shenzhen Stock Exchange.

A year ago (2022), the worst stock index was China's ChiNext index. One year later (2023), the worst stock index is again ChiNext index.

In 2022, the bottom 10 stock indices were littered with the names of Chinese stock indices (ChiNext, A50, CSI300, Shenzhen Composite, Shanghai Composite). One year later (2023), the same Chinese stock indices appear on the bottom 10 list. New additions in 2023 on the bottom 10 list include Hong Kong's Hang Seng index and Hang Seng China Enterprise index.

Since the 2019 large-scale mass protests in Hong Kong, the Hang Seng Index has suffered an unprecedented 4 consecutive down years (2020 -3.4%, 2021 -14.08%, 2022 -15.46%, 2023 -13.82%)

For long-term investors, it may be a good time to buy some HK stocks to take advantage of the low valuation. A rebound driven by mean reversion is due. A lot of pessimistic HK investors who want to be out should be mostly out by the 4th down year.

For shorter-term traders who are usually momentum-oriented, who is to say a 5th consecutive down year cannot happen again, given the strong momentum? Momentum traders may want to wait for an initial strong rebound first, then get in.

The top 2 currencies in 2023 are exotic pairs - Mexican Peso USDMXN and Polish zloty USDPLN. I do not know much about them to comment.

Both the Mexican Peso and the Brazilian Real appeared in the top 5 currency list in the past 2 years (2023, 2022).

Bottom ranking of currencies versus USD in 2023

Bottom ranking of currencies versus USD in 2022

The worst currency in 2023 was the Argentina Peso USDARS (357.42%!). One year ago (2022), the worst currency was also the Argentina Peso. The countries making up the worst 4 currencies of both years are the same. These countries are Argentina, Turkey, Egypt and Pakistan.

What's common among these 4 countries with fast-depreciating currencies?

These 4 countries are among the top 10 countries with the highest inflation in 2023.

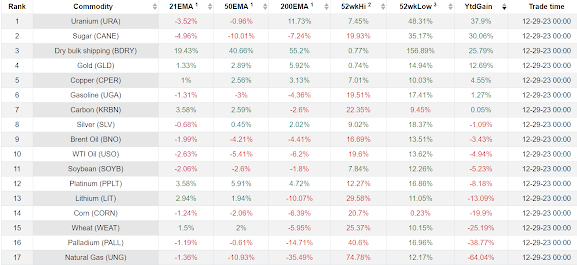

Ranking of commodities in 2023

2023 has not been a good year for commodities in general. Natural gas fell 64% in 2023. Unfortunately, it did not help much in lowering the electricity utility bill despite Singapore generating about 92% of its electricity from natural gas.

All the top 10 major cryptocurrencies in 2023 made triple-digit percentage gains. The top crypto Solana scored 922.44% gain. One year ago, Solana suffered a loss of 98%. Cryptocurrencies can be very profitable if you are a good trader.

The recovery in 2023 from 2022 lows was incredible for cryptocurrencies.

There have been several news reports about Singaporeans losing money to online hackers/scammers. SGD1.4 trillion has been lost to scams globally. Singapore victims lost the most on average. This is a risk we cannot ignore.

I will talk about the habits and practices I adopt to reduce this hacking/scamming risk.

Ensure smartphone settings are set to minimize security risk

The most dangerous device to be hacked in my possession is my smartphone. I guard my phone with the same level of security as I did for my rifle during National Service today.

Disable the "install unknown apps" option. It will prevent accidental installation of malware which allows scammers to gain access to your bank accounts. This is how you disable the "install unknown apps" option. Go to Settings. Search for "unknown". Then select the appropriate option. Make sure that all apps, especially browsers and messaging apps (WhatsApp, Telegram, SMS) are disabled from installing unknown apps.

This option should be disabled by default but do not assume. Check it out and confirm it has been disabled.

I did this for all my loved ones. Do this for your elderly parents because they are the most vulnerable group.

Do not install apps that are not from official app stores like Google Play Store (Android phones) or Apple App Store(iOS)

Most of the hacking incidents I read result from users installing an app not from the official app stores.

If you are using an Android phone, do not install any app not from Google Play Store.

If you are using an iPhone, do not install any app not from Apple App Store.

If phone users followed this simple rule, probably 90% of the hacking incidents I read about would not have happened.

Don't install apps unnecessarily even if they are from the official Google Play store

Less is more when it comes to phone security. The fewer apps installed, the lesser the risk of being hacked.

There is no guarantee that the official app stores can screen off all the apps with malicious intent. Here is a list of criteria I use before installing an app from Google Play Store

Apps are from large, reputable companies(Google, Microsoft) or government agencies

Obviously, these organizations will not steal your money.

More than 100,000 downloads

If the apps do not meet the first criteria, then they should have at least 100,000 downloads. Most of the apps I have on my phone have more than 1m downloads.The greater the number of downloads, the lower the risk of them being malware.

use biometric (or fingerprint), not password, authentication

Malware can intercept passwords as you type them but it cannot if you authenticate using your fingerprint.

Whenever I have the option to use fingerprint authentication, I will do so. I will not buy a phone which does not support fingerprint authentication.

Enable app notifications on banking/financial services

I enable notifications on all financial transactions as much as possible. I go to all the banking, credit card, brokerage, and money-related websites I use and ensure that the settings are made in such a way that the smallest financial transaction will trigger an alert to my phone and/or send an email.

This way, I can take immediate action when a hacker starts stealing my money.

Switch the phone off or put it into airplane mode when I'm sleeping

If a hacker managed to gain access to the phone, the most likely time to steal is during the victim's sleeping hours. If the hacker tries to steal during the day, the app notifications will alert the victim.

By switching my phone off or putting it into airplane mode, the hacker cannot steal my money while I am sleeping.

Avoid answering incoming phone calls starting with “+” sign prefix

Most of the incoming phone calls starting with “+” sign prefix are automated calls which are likely scam calls. The moment I hear an automated voice, I hang up the phone.

I do not answer incoming calls from an unknown number unless I am expecting an important phone call.

Avoid clicking on links in SMS

Clicking on phishing links in SMS can lead to accidental malware installation, if the "install unknown apps" option is not disabled.

I installed the Scam Shield app from Singapore Police Force to reduce the incidents of scam calls and scam SMSes.

Scan phone, PC/laptop at least once weekly for virus/malware

I set a calendar event to remind myself to scan for viruses/malwares on my phone and computers to do this at a specified time each week. I try to do this with discipline without fail so that in time, it becomes an ingrained habit.

Please share these practices around if you think they make sense and are helpful.

In an earlier post, I wrote about how I made a stable income on FTX before the whole fraud unravelled. It is easy to learn the wrong lessons in investing because an investor can make money despite being very wrong. Customers of FTX who escaped with some profits should not gloat about it. They were wrong and should count themselves as lucky. I was lucky. Regardless of whether the outcome was good or bad, this disaster calls for post-mortem reflections.

Right till the end, I never suspected Sam Bankman-Fried (SBF) to be a fraud even when the bank run was intense. I was duped. Thankfully, I assumed that crypto was unsafe and was constantly on alert to look out for warning signs.

I registered as an FTX customer in 2021. From the beginning, there were already signs that something was wrong. When I wired money to FTX Blockfolio last year, the recipient was "Alameda Research". Alameda was SBF's hedge fund. SBF was the biggest shareholder of both Alameda Research and FTX. At one time, Alameda was the biggest trader on FTX. This was a huge conflict of interest. Although Alameda was the main market maker in FTX, SBF had long insisted that the two businesses operated independently of one another. How can the two businesses be independent of each other when both can access the same bank account?

I chose to ignore this warning sign. As long as FTX does not go bankrupt, my delta-neutral positions at FTX will be safe. My main concern was counterparty risk. SBF doing shady stuff with Alameda does not affect my style of trading as long as FTX is financially sound and in no danger of collapsing. It was not unreasonable to expect some shady business in an unregulated industry, particularly one that deals with money. I was prepared to take this risk.

There was something about SBF that made me worried. He appeared on the cover of several prominent business news magazines. There have been past instances when appearing on the cover page marked the peak of a CEO's career. In some cases, the CEO turned out to be a fraud! Hello, Elizabeth Holmes and Sam Bankman-Fried.

I even warned SBF on Twitter about the cover page curse 3 months before the collapse out of concern for my money on FTX. He probably did not notice as I am a nobody.

I monitored FTX news on Twitter closely. If you want up-to-date news about crypto, Twitter is the place to go, not mainstream media. By the time news hits mainstream media, it is too late.

One fine day on Twitter, I came across this news article from Coindesk. It rang the loudest alarm bell about FTX. Alameda had a highly questionable, weak balance sheet. On the surface, the balance sheet looked fine with $8 billion in liabilities backed by $14.6 billion in assets. On closer look, much of its assets were FTT tokens and FTT are printed by FTX itself. $2.16b of the FTT was used as collateral and if the price of FTT crashes, Alameda will be liable for a big margin call. If Alameda falls, the contagion will spread immediately to FTX given their close links.

Now, I had a useful and easy reference point to monitor FTX counterparty risk. This critical reference point was the FTT price. If FTT starts to fall at a worrying pace, get the hell out of FTX. I relied on Luna and UST prices as warning signals to get the hell out of Anchor. Relying on market signals to get out of danger has saved me several times in the past and it did not fail me this time. This explains why my blog name is "Market Observer".

In hindsight, I should have withdrawn my funds from FTX when the negative news article from Coindesk was released but I did not. The lending rate of some coins in my crypto portfolio spiked up around that time. I remembered DOGE lending rate at FTX.US even shot up to 2000% during one particular hour near the end of October. The funding rate for perpetual futures also went positive. I was earning good interest from both lending spot tokens and shorting perps in my delta-neutral trades.

Before the FTX collapse, FTT had a relatively smaller price fall than other cryptocurrencies in the crypto bear market. The relative price strength of FTT gave me some confidence that Alameda was safe at the moment. I decided to wait for SBF's response to the damning Coindesk news article which was published on Wed, 2 Nov 2022. By Sunday, there was still no reaction from SBF. The part that made me most nervous was that the FTT price had started falling fast. Between Saturday afternoon (5 Nov 2022) and Sunday afternoon (6 Nov 2022 Singapore time), FTT fell more than 10%. This is a large amount compared to its normal volatility.

At this point, I decided to get the hell out of FTX on Sunday afternoon.

One alarming aspect of Alameda's balance sheet was that the sheer amount of FTT held on Alameda's books itself exceeded the total market capitalization of FTT in public circulation. Alameda and FTX had an interest in supporting FTT price. They certainly were not selling FTT. I believe most retail investors' FTT holdings were staked at FTX to enjoy lower commissions and other platform benefits like mine. So, they cannot be the ones selling. I wonder who was selling down FTT that weekend to cause the rapid price fall. Whoever it was, it was probably a big whale. The answer was out by Sunday night.

With a small public circulation and a large whale who wants to sell out everything, FTT was toast.

When CZ's tweet triggered a bank run on FTX, I was not out yet. It took me several hours to unwind my delta-neutral positions on FTX. I had to unwind bit by bit to get a good exit price and each time, I had to wait for the right trading set-up to exit. I slept only 2 hours that night.

I was only able to withdraw a fraction of my funds from FTX to my DBS bank account. Most of the money was still stuck in the withdrawal process as reflected on FTX webpage after 12 hours. By this time, there was an intense bank run going on. My body was shaking.

My engineering training instilled in me the good habit of building redundancy into a system to ensure reliability. Always have backup systems ready. Thus, I had other crypto exchange accounts as a ready backup for fund deposit in case I want to withdraw funds from FTX urgently one day. I turned to withdraw the funds to my backup crypto exchange accounts instead of the DBS account. Again, the withdrawal was always stuck in progress on the FTX webpage. My heart rate shot up.

I took a few deep breaths. I remembered when I was self-learning how to write smart contracts, I could view coin withdrawal status on the blockchain. When I looked at the transaction status, it said something like "Error. Insufficient funds." Hmm ... maybe the amount I tried to withdraw was too large. So, I cancelled the withdrawal ticket on FTX and initiated another withdrawal with a much smaller amount. This time, the withdrawal went through after waiting for about 15 minutes. I still remembered this was on Monday night (7 Nov 2022 SG time). By withdrawing bit by bit each time, I managed to withdraw most of my funds by the next morning (8 Nov 2022 SG time).

I could have withdrawn everything but I did not. Why didn't I?

Just 1 week before the FTX collapse, FTX made an announcement that caused me to believe they were not scammers running a Ponzi scheme.

Prior to this announcement, customers were earning a 5% yield on the first USD10m worth of cryptocurrencies in the FTX Earn programme. With this announcement, the 5% yield is limited to only the first 100k. Big whale customers who had millions in their FTX account to enjoy the 5% yield would be withdrawing down to $100k since the yield has dropped to zero beyond $100k. I thought if FTX were running a Ponzi scheme, they would not have made this policy change as it would cause a mini bank-run among their whale customers. Ponzi scammers will be hatching plans to attract more funds instead. Hence, I deliberately left some funds on FTX even though I could have withdrawn everything during the bank run that caused their collapse. My funds are now stuck and I have written them off to zero.

Many people thought CZ's tweet was the trigger that caused FTX's collapse. Sometimes, I wonder if the tweet announcement on the FTX Earn 100k limit was the one. FTX will be vulnerable to a bank run after this announcement because the whales will be withdrawing. If an enemy is waiting for an opportunity to strike, this will be it. The very next day on 2 Nov 2022, Alameda's weak balance sheet was leaked in a news article, highlighting how vulnerable they were on FTT token price. 4 days later, a major competitor struck at the heart of FTX's weakness by announcing they are selling down their FTT holdings. 5 days later, FTX declared bankruptcy.

I am not implying that this enemy caused FTX to go bankrupt. CZ was the trigger, not the cause. The root cause was SBF himself.

I am still puzzled today why FTX made this policy change to limit the 5% yield to the first $100k. Hopefully, someone can explain this mystery to me one day.

FTX has been exposed as a fraud and is now bankrupt. I have lost my funds on FTX, although I withdrew most of it before the collapse. I owe it to myself to reflect deeply on this event. I also owe it to my readers because I wrote 2 positive articles(1, 2) on FTX in the past. I was not paid a single cent for writing the articles. I wrote them on this financial blog because I was a happy customer of FTX.

Some people gloat over the investment losses of others. Some people get resentful when others are profitable. I do not wish to indulge either group. Hence, I do not wish to talk about how much I eventually made or lost from FTX. This information is relevant only to me. The important content is the lessons to be learnt from this disaster.

Why was I so enthusiastic about FTX? My experience with FTX has been wonderful until the fraud unravelled. I was making a stable income on the FTX platform in the bear market of 2022 when every asset class lost money. I confess I am a selfish person. I cannot reveal in detail how I did it on FTX when the strategy was still working to avoid returns from being driven down. I do not mind revealing it now since FTX is gone.

How I made a stable income from FTX in 2022

Previously, I wrote favourably about the lending feature of FTX. Users can enjoy good yields by lending out their crypto assets on FTX. However, this alone is not enough to provide a stable income. You can lend out for 20% yield but if the crypto asset crashes 50% (and most did in crypto winter 2022), you will still sustain heavy losses. To solve this problem, I shorted the underlying crypto assets through perpetual futures on FTX. This way, I will not lose money regardless of whether the cryptocurrencies are moving down or up. This strategy is known as delta-neutral trading. It is common knowledge. Nothing special here as most crypto traders knew about it.

The secret ingredient was FTX.US

FTX.US had consistently higher lending rates for some crypto tokens than FTX.com. I think this market inefficiency existed because Americans had difficulty accessing perpetual futures due to regulatory restrictions. Many non-Americans are not aware of FTX.US because they thought it is mainly for Americans. The crypto offerings at first glance are inferior to what is available on FTX.com. Many non-Americans will not take a closer look.

To find out which are the crypto tokens with high lending rates on FTX.US, I wrote software using FTX API to monitor the lending rates on FTX.US

After identifying the tokens, I bought them in the spot market and shorted the equivalent amount with perpetual futures on FTX.com. The tricky part about shorting perpetual futures is the funding rate. When the funding rate is negative, shorts have to pay. When the funding rate is positive, shorts get paid. A good situation is when the delta-neutral trader gets paid for both lending out the spot tokens and shorting the corresponding perpetual future. Unfortunately, in the crypto bear market of 2022, most perpetual futures traded with negative funding rates because shorting is more prevalent in bear markets. To identify the tokens that traded with favourable funding rates for shorting, I wrote software to monitor funding rates on FTX.com using FTX API.

When the funding rate gets too negative to the extent that the delta-neutral position starts to lose money, I will unwind the position. This in and out action can lead to high commission. Fortunately, FTX has this promotion that reduces maker fees to zero if the user staked enough FTT tokens (I lost all the staked FTT when FTX collapsed). In other words, if I place a limit order and wait for the order to be filled, the fee paid is zero.

The trickiest part I faced in the delta-neutral strategy was executing the trades to enter and exit the positions. To take advantage of zero maker-fee orders on FTX, I had to place limit orders and wait for orders to be filled. I had to determine whether I should buy first, then sell or sell first, then buy. Sometimes I made and sometimes I lost. I am no longer able to access my FTX account, so I cannot find out whether I made or lost in the end from these executions. I enjoyed the market challenges and gained some day trading experience(Day trading is something that I would not recommend to most people) as a result.

FTX did not charge fees for withdrawals unless they took place on Ethereum blockchain. I was able to move tokens free of charge between FTX.com and FTX.US using the Solana blockchain.

When I could not find good trades for the delta-neutral strategy on FTX.com and FTX.US, I will place my USDC stablecoins in Blockfolio app to earn 5%-8% yield in the FTX Earn programme. Funds in Blockfolio can be withdrawn at any time when I spot delta-neutral opportunities.

In a bear market year when all asset classes fell, low-risk income from delta-neutral trading was a godsend until the FTX fraud unravelled.

I will stop here for the moment. In part 2 of the article, I will cover my self-reflections on the FTX fiasco.

Here are the results of financial markets that I track for 2022.

Top ranking of stock indices in 2022 (USD-adjusted)

The ranking of the stock indices is adjusted to USD. An investor can make good gains but the gains can be lost from a depreciating currency. Investors cannot ignore currency movements. Ignoring them will lead to a distorted reflection of the purchasing power made from their investment gains.

2022 has been a sea of red for stocks worldwide, as can be seen from the year-to-date performance of global stock indices. It is an achievement if you managed to break even this year in your stock portfolio.

Straits Times Index(STI) is the pride of Singapore in the terrible bear market of 2022. STI is ranked 3rd in 2022, though the 4.77% annual gain is not impressive considering the risk involved. Today, one can easily get almost risk-free gain of above 3% from 12-month bank fixed deposits and Singapore Savings Bonds.

The number one stock index performer goes to Turkey's Borsa Istanbul 100 which gained 111% USD-adjusted. It gained almost 200% in nominal terms. One distinguishing feature in Turkey's economy in 2022 is high inflation and tumbling currency. Inflation reached as high as 85.5% and the currency tumbled 29% against USD. I think the strong stock market gains were strongly driven by Turkish investors using stocks to protect against the ravages of high inflation and a weak currency.

Bottom ranking of stock indices in 2022 (USD-adjusted)

The worst-performing stock indices in 2022 are related to technology stocks. The worst 2 are Chi-next(tech index of China) and Nasdaq100(tech index of U.S). Bottom 3rd and 4th are Korea's Kospi200 and Taiwan's TSEC weighted index. Korea and Taiwan are countries strong in technology product exports to the rest of the world.

Top ranking of currencies versus USD in 2022

USD was already strong last year (2021) and its strength continued into 2022. 2022 is the year of the U.S. dollar, thanks to the Federal Reserve's moves to raise interest rates aggressively to fight inflation. The onslaught caused most currencies to depreciate against the USD in 2022 except commodity-based currencies and the Singapore dollar. Like Straits Times Index, the Singapore dollar(SGD) made Singaporeans proud again. Singapore is the only country with no commodity export that has an appreciating currency against the USD in 2022.

Singapore does not set its own interest rate. The central bank, MAS, relies on fixing the exchange rate to fight inflation and it did well. With Singapore's strong reserves, I am confident SGD should be one of the stronger currencies that can weather the onslaught of a strong USD.

Bottom ranking of currencies versus USD in 2022

Japanese Yen was weak last year (2021) and its weakness continued this year. Last year, it dropped 11.47% against USD and it continued to tumble 12.2% this year. It used to be a safe haven currency which will rise in a bearish year for stocks like 2008. This year, it did the opposite. The weak Yen should make Japan a cheaper place for tourists to visit.

Besides enjoying a relatively strong stock market and currency in 2022, Singapore's housing market defied the global real estate downturn caused by soaring mortgage rates. This is despite strong, consistent government measures in the form of taxes and lending restrictions over the years to curb rising property prices.

While it is impressive that the major asset classes such as stocks, currency and real estate in Singapore have done relatively well in bearish 2022, I would rather see the Singapore property market tumble from the top rankings. This is nothing to be proud of. High property price is a major cause of the high cost of living in Singapore. It imposes a high social cost on young people and young couples. High mortgage debt and unaffordable housing cause youngsters to lose hope for the future. It discourages them to have kids and the sense of hopelessness may cause some of them to lie flat. People who lose hope for the future stop working hard.

I do not think rising property prices are a good thing. The real estate investment gains enjoyed by the older generation are offset by the higher cost of living imposed on the younger generation. Young people are our future and if they feel bleak about the future, we have no future. Although I am not affected by rising property prices as a property owner with no mortgage debt, rising property prices will still affect me. When my kids grow up and they struggle with rising property prices, their problem will become my problem.

I expect high property taxes and lending restrictions on property purchase in Singapore to continue as the government is aware of the social cost caused by high property prices.

Ranking of commodities in 2022

2022 was a good year for commodities. Unfortunately, this was a major factor that contributed to inflation. Energy prices made good gains in 2022 with brent oil rising 35%. What is interesting is how much energy prices have come down from the 52-week high. Oil prices have slid more than 22% from the 52-week high. Natural gas prices are down more than 58% from 52-week high! Energy commodities are already in a bear market. This is telling us that commodity prices are finally coming down as a result of the slowing economy squeezed by high interest rates. This is a sign that inflation may be coming down.

Ranking of cryptocurrencies in 2022

Cryptocurrencies are in a sea of deep deep red in 2022. The top-performing major cryptocurrency is TRX and it is down by 28%. The rest of them are down by more than 50%! I myself had narrow escapes with crypto investments (Anchor/UST, Hodlnaut, FTX) that caused almost 100% loss to investors who did not exit in time.

I believe the asset class that caused the most damage to investors, especially big institutional investors, in 2022 are fixed income long-term government securities.

Ironically, the 20+ year Treasury bond which is supposed to be risk-off fell more than risk-on S&P500 during Oct.

This asset class is a strange world to me. It moved from a strange world of negative yield to another strange world where yields rose so much so fast that risk-off assets(Treasuries) lost more money than risk-on assets(stocks) in a risk-off year. I cannot comment much on a world which I find strange.